Canadian Dollar Monthly Update June 2019

Economic Outlook and Summary

Federal Reserve Chairman Powell has signaled the Fed will look to cut rates, if necessary, in 2019 and it looks like they are prepared for U.S President Trump’s trade war and the implications of it on the U.S economy. Expectations around the Federal Reserve believe to be that there will be a rate cut at some point this year as the growing fear of recession could lead to multiple rate cuts moving forward. USD has been through a period of appreciation recently due to ongoing trade talks with China and the uncertainty that is stemming from this political trade war. Global investors will be hoping a trade agreement is on the way and are hopeful for the stars to align at the G-20 meeting taking place at the end of June 2019.

The Canadian economy has looked to rebound since March 2019, compared to the end of 2018 which encountered slower growth and was a period of downturn for the CAD. Canada’s major macroeconomic indicators has showed positive signs as housing starts, home resales, manufacturing shipments and various employment data all receiving strong momentum and gains. The first four months of 2019 have been great for jobs and unemployment as job creation was potent and better than the last five years over the same time period. Analysts believe business investment should look to carry the Canadian economy and drive the rebound through 2019 and 2020, however trade disputes with the U.S could cause uncertainty with investments that are poured into Canada. Crude oil had a terrible month of May, experiencing the biggest loss in the last 2 quarters which totalled around 6%. U.S President, Donald Trump, has also shifted his trade and tariff disputes over to Mexico and is considering adding tariffs to all Mexican goods.

The US dollar and the Federal Reserve

The greenback suffered a bad start to the year as poor growth and scandals hurt the US dollar. U.S.-China trade tensions continued to dominate headlines with President Trump stating that the U.S. is ‘not ready to make a deal’. China has responded to the U.S with both direct and indirect threats by suggesting that they too may influence global supply chains through their dominance of ‘rare earth’ exports – a group of 17 minerals used in the production of most modern electronic devices. A ban on exports to the U.S. could disrupt production and affect prices of many electronic products. In other trade news, President Trump threatened to impose a 5% tariff on all Mexican imports starting June 10th. The move is aimed at stopping illegal immigration, and the tariff rate could be raised to 25% by October 1, unless Trump deems illegal immigration has been remedied. Investors have little choice but to adhere to the risk aversion theme while U.S.-led trade tensions can unpredictably open new fronts and affect sectors beyond trade.

At a conference in Chicago, Federal Reserve Board Chairman Jerome Powell has signaled that the Fed will cut interest rates if necessary. He said he was prepared to respond to the Trump administration’s trade conflicts to protect the U.S. economy. Expectations are rising that the Fed will cut rates at least once and possibly twice before this year’s end in response to the growing risk of a recession. The Fed is conducting its first-ever public review of its operations and will focus on ways to improve its rate strategies, the tools it uses to achieve its objectives and the way it communicates its actions to the public. After this outreach, Fed officials will begin using their regular meetings to discuss possible changes.

The Canadian Dollar and Bank of Canada

The Canadian dollar underperformed against the USD for the fourth consecutive month in the month of May. In the month of May, the CAD fluctuations brought it to the point of selling off and major recovery within the space of a few days. Bank analysts predict a limited downside for the Canadian dollar in the months ahead, mainly due to a weaker outlook on the USD. Analysts have also downgraded the outlook for the CAD in a modest measure which is a result of weak GDP growth lingering trade war headwinds. Canada and its currency are heavily reliant on capital inflows to finance a chronic current account deficit which is over 3% of GDP in the first quarter. As Canada and its economy would love for higher levels of Foreign Direct Investment (FDI) unfortunately those levels have not been attained and FDI has been negative last 3 out of 4 quarters. Interest rate spreads between Canada and U.S have narrowed substantially as U.S yields retreated in recent weeks. Strong job reports of Canadian employment did not show any real affect on the CAD falling out of line with expectations. Bank of Canada did attempt to rally investment with their measured statement late this quarter, however investors do not seem motivated to do so. Even with the central bank acknowledging the improvement in financial data, it did elect leave interest rates unchanged, which is understandable due to the threats posed by ongoing global trade issues.

Oil Prices

Crude oil markets had a brutal month of May, experiencing the biggest loss in six months which ended with a massive 6% drop on the final day of the month when US President Donald Trump tweeted about imposing a 5% tariff on all Mexican goods. Markets were left reeling from the announcement since Mexico is one of the largest U.S trade partners and a major supplier of crude oil. Crude oil was coming into the month of May holding a bullish trend that started December 2018, but sellers came back with aggression to erase majority of that topside ramp. Concern of rising US gasoline stockpiles which suggest weakening demand will frame the upcoming OPEC meeting in June as a pivotal event that will shape oil’s outlook for the rest of the year. However, a decision by OPEC+ producers to extend their supply cuts campaign into the second half of 2019 may not be enough to fully support oil prices, should global demand deteriorate further.

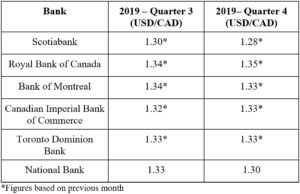

FX Forecast Table June 2019

Click Here to Subscribe